- Home > Blog > Small Business Financing > How Small Business Loans Work

How Small Business Loans Work

Small businesses are integral to the success of the U.S. economy. According to the Office of Advocacy Report in 2022, they account for two-thirds of the jobs added to the economy over the last 25 years. But small businesses are also prone to high failure rates. Forbes.com reveals that only one out of two small businesses makes it to the 5-year mark, and only one out of three sustain in business for 10 years or more.

The point is that small businesses are both important and potentially fragile. Many require funding to cover an array of issues, such as startup costs, cash flow challenges, or expansion. Small business loans are one of several funding options you have as a small business owner. This article explores what these loans are and how they may help your company.

What Is a Small Business Loan?

As the name implies, a small business loan is any loan that a lender offers to small business owners to utilize for the growth and day-to-day operation of their company. Many of these loans come with backing from the Small Business Administration (SBA), though this isn’t a requirement for the loan.

You can get these types of loans from commercial banks and many online lenders. While most banks offer SBA-backed loans, they tend to have a tedious approval process and middling approval rates. On the other hand, online lenders may not always have SBA backing, but they often have more lenient borrowing criteria and a faster fund transfer process.

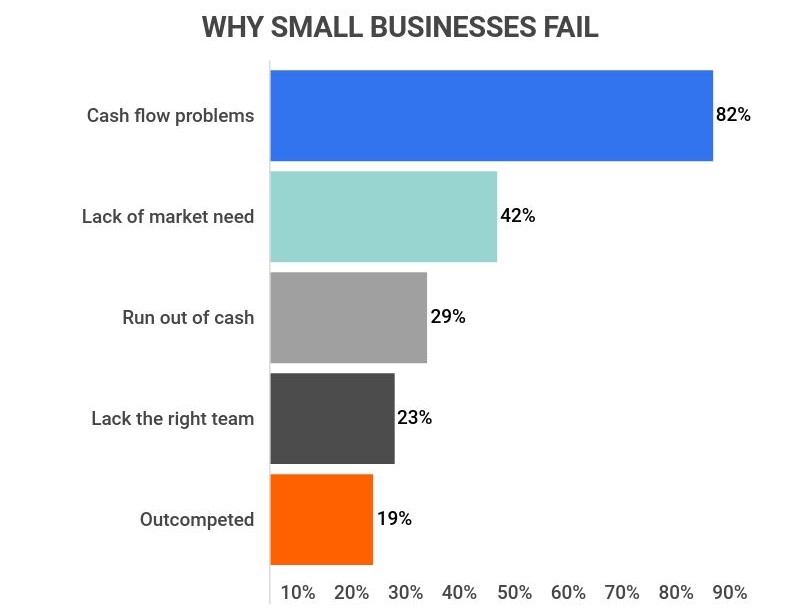

Why Do Small Businesses Need Business Loans?

There are many reasons why a small business may fail. According to data from Zippia, cash flow problems play a role in 82% of business failures. In 42% of cases, a lack of market need for the company’s product plays a role in the downfall, while simply running out of money is the reason for 29% of small business failures.

{kind=link}

Small business loans can solve the financial issues that plague so many companies.

Some of the most common uses for small business loans include the following:

- Financing equipment purchases

- Business expansion or growth

- Product research and development

- Maintaining a healthy cash flow

- Marketing

- Managing inventory

- Covering seasonal or periodic sales issues

- Debt consolidation

- Hiring and payroll

Types of Small Business Loans

You have several funding options when applying for small business loans. The following are the most common types.

Working Capital Loans

Working capital loans help small businesses to cover their day-to-day expenses. They’re typically used to fund operating costs and similar business expenses, such as payroll, rent, utility bills and vendor invoices. Some companies also find them useful for covering slow sales periods. Read our article for more information on how to get working capital loans.

Line of Credit

With a line of credit, your lender sets a credit limit. You can draw from the available credit, up to that limit, to fund anything your business needs. You only make repayments on the money drawn, rather than your credit limit. These loans are ideal for small businesses that need flexible access to funding.

Short Term Loans

A short term business loan covers a company’s immediate financial needs. They will typically have short repayment periods, with 12 to 18 months being common. You may also pay more interest on these types of loans than you would on others. However, they’re ideal for solving temporary cash flow issues, assuming you’re confident that your business can handle the repayments.

Equipment Financing

As the name implies, equipment financing is a type of loan dedicated to helping your company buy or lease equipment. In most cases, the equipment you buy serves as the collateral on these loans, meaning you don’t have to use any other assets. If you default, the lender claims the equipment to sell and recoup its costs.

Accounts Receivable

These loans allow you to borrow money against the value of your company’s accounts receivable, otherwise known as your unpaid invoices. The lender gives your company a percentage of the amount you have in accounts receivable as a loan or line of credit. The invoices serve as collateral, with repayment usually occurring once your clients pay their invoices. Read our blog to know the benefits of accounts receivable financing.

How Does a Small Business Loan Work?

Though every lender has their processes and criteria for small business loans, four common steps are usually followed:

- Application

- Approval

- Disbursal

- Repayment

Applying for Small Business Loan

Applying for a small business loan isn’t a simple case of sending in an application form. You have actions to take before the application process.

These actions include researching different lenders to find one that offers a loan that’s suitable for your needs. Once you’ve found the right lender, you must gather the appropriate financial and tax documents, which may include the following:

- Profit and loss statements

- Declarations of existing debt

- Income tax returns for the owner and any major shareholders

Some lenders also ask for a business plan so they can learn more about your company.

Assuming you have the appropriate documentation, you need to figure out which type of loan works best for you and how much you need to borrow. Both these decisions are critical as the wrong choice could lead you to a loan that’s too big to repay comfortably or doesn’t serve your company’s needs.

Once you’re certain you have everything you need, you apply based on the lender’s application process.

Approval of Small Business Loan Application

Once the lender receives your application, it goes through an approval process. Here, the lender looks for red flags that may suggest that your business is a risky borrower. These red flags include:

- A low business or personal credit score

- High debt-to-income ratio

- Poor profit figures or projections

Furthermore, lenders may get cold feet about a business if it’s brand-new or if it’s in a risky industry, such as gambling. In these cases, specialty lenders that offer industry or business-specific loans may be a better choice than lenders offering small business loans.

The lender uses this information to build a risk profile for your business. Based on the risk you present, the lender decides whether to approve your application, how much to lend and the conditions it attaches to the loan.

Disbursal of Loan Amount

Upon approving your application, the lender sends the terms and conditions for its loan to your business. This document informs you of the loan’s repayment cycle, term period, and the interest rate attached to the loan. Assuming you’re happy with the terms you’ve received, you sign for the loan and receive the funds.

How you receive the funds varies depending on the type of loan. In most cases, you either receive a lump sum payment or receive the funds in installments, based on the loan’s terms. However, a line of credit is different because you receive access to funds based on a credit limit. You can draw from those funds up to the limit, with repayments varying depending on how much you’ve borrowed.

Repaying the Small Business Loan

Repayment conditions vary depending on the type of loan.

With most small business loans, you make daily, weekly, biweekly, or monthly payments. Some loans have set repayment amounts, with interest applied. Others, such as a line of credit, require you to make repayments based on how much you’ve borrowed.

Accounts receivable loans work differently because you’re using your unpaid invoices as collateral on the loan. The lender essentially receives the money from the invoices used as its repayment, meaning you don’t have to make periodical repayments.

Defaulting on your small business loan can create several problems. These range from placing a black mark on your credit record, making other lenders unlikely to lend to your company, to a lender claiming any assets you’ve used as collateral on the loan.

FAQs

What happens if I don’t repay my small business loan?

The consequences for failing to repay your small business loan vary. If you’ve used an asset as collateral, your lender may claim that asset to serve as repayment. Furthermore, missing repayments makes it harder to get loans in the future as lenders are less likely to trust you as a borrower.

How are small business loans paid back?

You repay a small business loan based on the type and terms of the loan. Most require periodic repayments, often of set amounts. Other types of loans have varying repayment amounts based on what you borrow, such as with a line of credit.

Can you get a business loan with no revenue?

You’re unlikely to get a small business loan from most lenders if you have no revenue. In these cases, it’s better to apply for a startup loan, which is tailored specifically for companies that are just starting out and thus have no customers.